Way back on the 16th November a Facebook discussion sent me on this weird, wild and wandering journey, creating posts on various political topics. I started with explaining why being a leftist isn’t the same as being a communist. Then proceeded with looking at if declining educational funded fueled political divide? Then had a quick butchers at Income inequality and Political attitudes, took a side route via the history of Uk voting regulation, the impact of longer life expectancy, before opening a post on the UK National Debt with a statement about how I was interested in whether the sale of the nation’s assets generated value or not, guess what — we have now reached the post on the UK’s Privatisation of nation assets…

A conversational look at the UK’s privatisation experiment — who gained, who didn’t, and why it matters.

In the late 1970s, Britain embarked on a grand economic adventure: selling off the nation’s publicly owned industries. Harold Macmillan famously called it “selling the family silver.” In hindsight, he was being generous.

By the end of the 1990s, the UK had flogged not just the silver, but the dining table, the carpets, the utilities, the rails, half the sky, and the rights to every tap in England.

The question is no longer “Was privatisation good or bad?”

It’s “Who actually benefited — and why did the public end up paying more for less?”

Let’s take a conversational, slightly blunt tour through the biggest wealth transfer in modern British history.

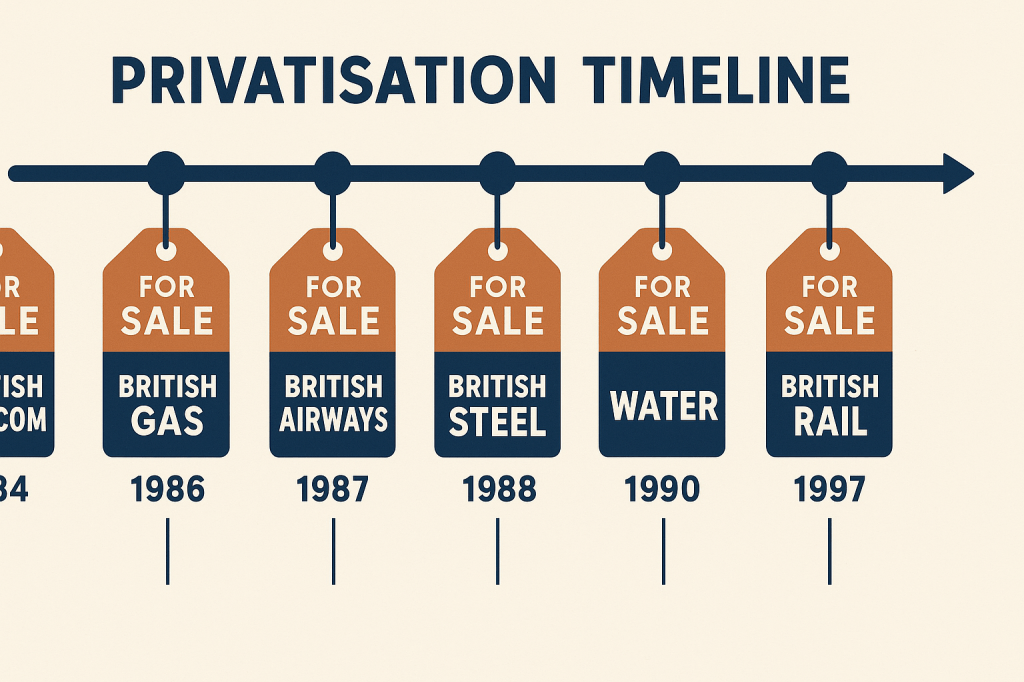

What Exactly Did Britain Sell?

Between 1981 and 1997, the UK sold almost everything you’d expect a functioning state to own:

Major industries:

British Telecom, British Gas, British Steel, British Airways, British Coal, British Rail (in pieces), British Petroleum, British Aerospace, British Energy, British Technology Group, British Sugar, Associated British Ports, British Shipbuilders, British Waterways.

Electricity:

Generation (National Power, PowerGen, Nuclear Electric), the National Grid, and all 12 regional electricity companies.

Water:

All of England’s water and sewerage companies — Anglian, Thames, Severn Trent, Wessex, Yorkshire, and so on. (Scotland, Northern Ireland, and Wales said “no thanks,” and kept theirs public.)

Transport:

British Transport Hotels, Sealink ferries, Travellers Fare, and eventually the highly fragmented rail system.

If it wasn’t nailed down, it went into a prospectus.

What We Were Promised

The ideological sales pitch was simple:

- Prices would fall

- Competition would magically appear

- Services would improve

- Efficiency would soar

- The government would cut debt

- “Popular capitalism” would flourish as millions bought shares

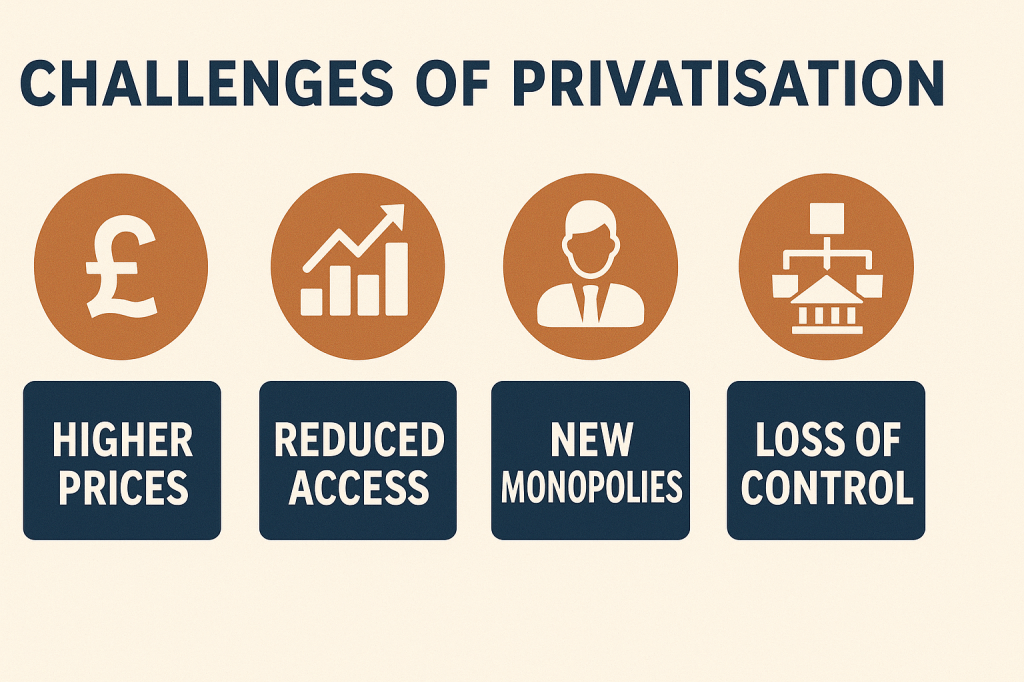

Forty years later, most of those promises have aged about as well as a lettuce in a heatwave.

Independent reviews from the National Audit Office, House of Commons Library, OECD, and academic studies (e.g., the Transnational Institute and Centre for Public Impact) show a consistent pattern:

prices rose faster than inflation;

investment lagged;

services deteriorated;

debt wasn’t reduced;

competition rarely materialised;

and shares rapidly concentrated in the hands of large institutions.

So… if the public didn’t win, who did?

The Real Winners of Privatisation

Now we get to the part no politician likes to talk about.

The City of London — First in Line, First to Profit

Privatisation created a gold rush for investment banks, underwriters, brokers, and financial advisers.

Most major share offers were significantly underpriced, as later acknowledged by the NAO and Parliamentary research. This guaranteed:

- instant, risk-free profits for institutional investors

- day-one price jumps

- enormous underwriting fees

The public were technically “invited to the party,” but the City drank the champagne before the doors opened.

Shareholders — But Not the Millions We Were Told About

The great dream of “popular capitalism” lasted about six months.

Yes, millions bought shares.

But millions also sold them quickly.

By the late 1990s:

- the majority of shares were owned by pension funds, banks, asset managers, and foreign investors

- individual ownership collapsed

- dividend payments exploded — flowing overwhelmingly to wealthy households and institutions

This wasn’t a people’s capitalism.

It was institutional capitalism with a friendly public-relations hat on.

Executives and Senior Management

One of the most reliable benefits of privatisation?

CEO pay packets expanding like they’d been watered with Miracle-Gro.

Post-privatisation:

- executive salaries surged

- bonus culture erupted

- stock-based incentives became the norm

- golden parachutes multiplied

If you ever wondered who privatisation was really designed for, you can start with the boardrooms.

Foreign Owners, Offshore Funds — and the Expensive Regulators We Created

Here’s the part most often forgotten:

When we sold off essential utilities, we didn’t just hand them to private companies — we handed them to private monopolies.

And monopolies need regulators.

So the public now pays for:

- Ofwat (water)

- Ofgem (energy)

- Ofcom (telecoms)

- Office of Rail & Road (rail)

- Industry-specific oversight teams and advisory panels

This regulatory ecosystem costs hundreds of millions annually — money we never had to spend when the industries were publicly owned.

And here’s the kicker:

The regulators were deliberately created weak.

The contracts used to privatise utilities were:

- ideologically light-touch

- poorly enforced

- legally favourable to corporate owners

- not designed to recover value for the public

- unable to prevent asset-stripping, debt-loading, or dividend binges

Meanwhile, foreign investment funds, private equity firms, and overseas state-owned utilities quietly bought up British companies — extracting profits while the public footed the bill for oversight.

We didn’t just privatise our assets.

We privatised the profits, and then paid to supervise the mess.

So… Did the Public Get Anything Out of It?

Short answer: not much.

Long answer:

- No debt miracle: The UK’s debt ratio rose sharply after privatisation, driven by economic cycles, not asset sales (OBR).

- Higher bills: Water, rail, and energy saw price increases far above inflation.

- Lower investment: Many privatised companies reduced long-term investment while increasing dividends (Ofwat, Ofgem).

- Infrastructure decay: Sewage spills, rail chaos, overloaded energy networks.

- Ongoing public subsidies: Rail now requires more subsidy than before privatisation (House of Commons Library).

Privatisation didn’t shrink the state.

It just made the public pay more for worse services.

The Great British Fire Sale — Why Assets Were Sold Cheap

This wasn’t strategy. This wasn’t long-term planning.

This was politics.

The mixture:

- ideological commitment to markets

- desire to weaken trade unions

- need to fund pre-election tax cuts

- City lobbying

- donor pressure

- a convenient way to create short-term “success stories”

Privatisation wasn’t a neutral economic decision.

It was a political project — designed to shift power away from labour, central government, and public institutions, and toward the financial sector and corporate ownership.

In other words:

It was never primarily about efficiency.

It was about who gets to control the country’s wealth.

What Happened Next?

Water: The Great Leakage of Public Value

England’s privatised water companies:

- loaded up with debt

- paid out huge dividends

- cut maintenance

- increased bills

- dumped sewage into rivers and seas (record levels – Environment Agency)

Meanwhile:

Wales’s not-for-profit model (Dŵr Cymru) reinvests all surplus into infrastructure and customer support.

Scotland and Northern Ireland?

Still public.

Better investment.

Lower leakage.

More resilience.

Rail: Higher Subsidies, Higher Fares

Britain’s rail network now receives more public subsidy than it did under British Rail — while delivering:

- higher fares

- fragmented service

- complex ticketing

- less accountability

Energy: Foreign-Owned and Under-Invested

The UK’s energy infrastructure relies heavily on overseas-owned utilities:

- investment lagged

- bills soared

- National Grid profits flowed abroad

- government repeatedly stepped in with subsidies

Competition?

Not really. Six companies dominated the market until very recently.

Telecoms: BT’s Underinvestment Problem

BT made shareholders happy for years — but underinvested in nationwide fibre rollout.

The UK’s broadband still lags behind international peers (Ofcom, OECD).

What If We’d Kept Them? (Just a Taste of the Counterfactual)

Instead of selling our national industries, we could have:

- generated stable long-term revenue

- reinvested profits in infrastructure

- borrowed against the assets during downturns

- kept bills lower

- avoided massive regulatory overhead

- ensured democratic accountability

Other countries — France, Norway, Singapore, Germany — kept far more public ownership.

Their infrastructure?

Generally better.

Their utilities?

More stable and less debt-loaded.

Their citizens?

Pay less for essential services.

Britain didn’t have to do a fire sale.

It chose to.

The Truth We Avoided for 40 Years

Privatisation didn’t fail because markets are bad.

It failed because it was designed to benefit shareholders, executives, and financial institutions — not citizens.

The winners:

- City banks

- early investors

- institutional shareholders

- foreign owners

- executives

- political donors

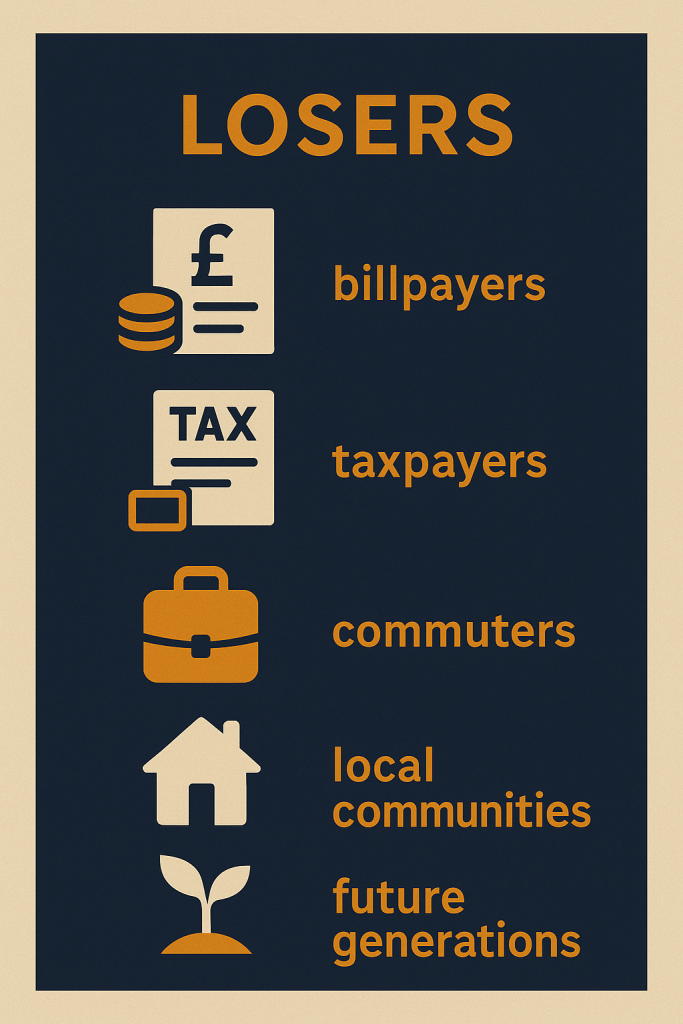

The losers:

- billpayers

- commuters

- taxpayers

- communities

- future generations

Britain didn’t just sell the family silver.

It sold the house, rented it back, and now pays extra whenever the pipes burst.

And the pipes burst a lot.

Relevant references/Other Interesting Reads

- https://www.tni.org/en/article/the-living-legacy-of-privatisation-in-the-united-kingdom

- https://centreforpublicimpact.org/public-impact-fundamentals/privatising-the-uks-nationalised-industries-in-the1980s/

- https://www.theguardian.com/commentisfree/2012/mar/29/short-history-of-privatisation

- https://www.economist.com/by-invitation/2023/07/10/mathew-lawrence-on-why-privatisation-has-been-a-costly-failure-in-britain?utm_campaign=shared_article

- https://researchbriefings.files.parliament.uk/documents/RP14-61/RP14-61.pdf

Discover more from Hysnaps Politics, Gaming, Music and Mental Health

Subscribe to get the latest posts sent to your email.