“And Why the UK Keeps Forgetting”

If people respond to incentives — and we do — then a system built around short-term rewards will encourage short-term behaviour, no matter how often everyone involved agrees to “do better next time”.

Not because the people involved are stupid.

Not because they’re greedy.

But because nearly none of us volunters to act against our own best interest — especially if it comes with a personal cost — no matter how good our intentions might be.

So the awkward question becomes:

How do we help systems stick to what they broadly agree they should be doing, even though we know they’ll tend to drift back toward familiar behaviour unless something actively encourages change?

We all know smoking is bad for us – and we all promise to stop – but most of us fail to do unless someone helps us.

We have systems of regulation, to actively encourage change and help protect against unintended consequences. And of course, like all of us, it is only as good at doing this as the tools it has available to use.

Regulation is not a moral judgement.

More like a brake pedal.

Not to stop the system.

Just to stop it accelerating indefinitely.

And a lot of the frustration around regulation comes from expecting it to do something it was never really meant to do.

Isn’t regulation supposed to stop people behaving badly?

You would think so, in fact most of us probably do think so.

But it’s not really how it works.

It doesn’t start from the idea that we can’t trust people. It starts from the much more mundane observation that pressure works,

There’s a great Terry Practchett line that sums this up rather neatly :-

“Unfortunately, the right words are more readily listened to if you also have a sharp stick”

– Jingo

Left alone, people tend to drift toward whatever earns them rewards fastest. In financial services, that often means speed, volume, and results that show up quickly.

Regulation is one of the few tools we have to slow things down a bit. To insert pauses. To force someone, somewhere, to ask:

“And what happens if this goes wrong?”

Sometimes that helps.

Sometimes it doesn’t.

And sometimes it just nudges behaviour into a slightly different shape.

But without it, systems have a habit of making a big noise and mess when they fail.

Why does regulation always seem to arrive after the damage is done?

Lol .. yep and that is really simple, as we all know rules almost always appear after something bad has happened – be it in the Financial Services, a sport, or everyday life.

The world isn’t a board game where the rules have been written upfront and nothing new can happen, unless you buiy the extension pack – but that is another matter.

There are no hard limits to how things can change. And there will always be people willing to see how far things can be pushed — sometimes for the good, sometimes for the not so good.

By the time a pattern is clear enough to regulate, it’s usually already embedded. Organisations have reorganised around it. Careers depend on it. Markets have adjusted.

So the poor old regulator often ends up trying to deal with yesterday’s behaviour while not breaking tomorrow’s system.

This is why it can feel reactive, awkward, and permanently behind the curve.

That isn’t always incompetence.

As we know it is much harder to get people to agree to follow rules to stop something that might happen, than it is to say –

“Look over there — when they did that thing, look what happened.

Thats why you really shouldn’t do it.

And if you do … well … remember my sharp stick.”

Often, it’s just timing.

Is this just a British problem?

Not really — but we do have our own rhythm.

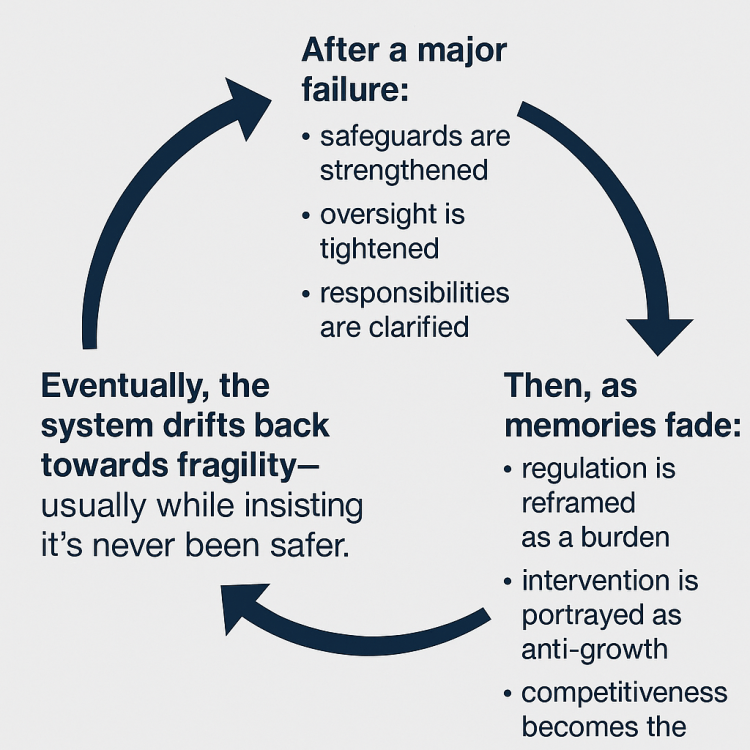

In the UK, financial regulation tends to move in cycles.

Something breaks.

We tighten things up.

Oversight improves.

Responsibilities get clarified.

Then, slowly, the mood shifts.

Rules start to feel inconvenient.

Oversight is described as a drag on growth.

Competitiveness becomes the overriding concern.

And gradually, the system drifts back toward fragility — usually while reassuring itself that it’s never been safer.

Other countries do this too.

We’re just seem particularly good at forgetting the last time.

Didn’t “light-touch regulation” make sense at the time?

This is the uncomfortable bit.

In the late 1990s and early 2000s, the UK didn’t accidentally end up with light-touch regulation. It chose it.

London was positioning itself as a global financial centre — flexible, innovative, open for business. Markets were assumed to self-correct. Institutions were assumed to understand their own risks. Regulators were encouraged to enable rather than challenge.

And for a while, that choice looked like it was working.

Growth was strong.

Tax receipts were healthy.

Banks were profitable.

Money flowed in.

But the calm was being bought in ways that only really show up later.

Banks borrowed more to boost returns.

They held thinner safety buffers.

Many relied on the same optimistic assumptions about risk.

And risks were bundled together in ways that quietly linked institutions beneath the surface.

The system looked stable because everyone was doing similar things.

Which, as it turned out, was the problem.

Were there warning signs we just talked ourselves past?

Not exactly.

Many of the decisions that mattered didn’t look obviously dangerous at the time.

Responsibility for system-wide safety was split across multiple bodies. No single organisation had the full picture. Warnings softened as they travelled. Accountability blurred.

Banks were allowed to judge their own risks using their own models. Complex products were created on the assumption that the players didn’t need close supervision, and wouldnt do something too risky.

None of this was illegal.

Much of it was encouraged.

Individually, these choices looked reasonable.

Together, they created something that worked very well — right up until it didn’t.

What actually happens when a financial system fails?

It doesn’t fail politely.

When things went wrong in 2008, the system froze. Payments, wages, lending — all suddenly at risk.

The government stepped in not to reward bad behaviour, but because letting the system collapse would have meant everyday life grinding to a halt.

So public money was used to stabilise banks.

Guarantees were issued to prevent panic.

Emergency funding kept the plumbing working.

At its peak, the support ran into the hundreds of billions, with guarantees well over £1 trillion.

Even after things were unwound, the cost to the public ran into tens of billions — roughly a thousand pounds per household.

Not as a bill anyone received.

But as risk we absorbed.

So who benefited — and who carried the risk?

In the years before the crash, the gains were fairly concentrated.

Senior staff were rewarded through bonuses.

Shareholders benefited from rising prices.

Governments enjoyed buoyant tax receipts.

Yes — governments too.

Those revenues were largely treated as permanent. They weren’t set aside. They became part of the baseline.

It was a bit like buying a car on hire purchase, covering the first year’s payments with a bonus, and quietly assuming you’d always get a bonus at least that big in future years.

When the bonuses stopped, the car didn’t go back.

The payments didn’t disappear.

You were still on the hook — just without the extra money you’d been relying on.

When losses arrived, they landed very differently.

Taxpayers absorbed bailouts and guarantees.

Workers faced recession and wage stagnation.

Savers and pension holders endured years of weak returns.

Public finances lost flexibility for a long time.

That wasn’t a moral failure.

It was how the system was wired.

Why does this keep sounding familiar?

All of this might feel safely historical. But like me, you may have noticed that some of the same arguements have resurfaced again..

That regulation holds back growth.

That oversight hurts competitiveness.

That innovation needs room.

That long-term risks can be dealt with later.

That doesn’t mean another crisis is inevitable.

But it does suggest we’re still very good at prioritising short-term gains while quietly deferring the consequences.

And history suggests those consequences rarely arrive gently.

So what is regulation actually doing here?

It isn’t about stopping markets from working.

It exists because markets amplify sensible behaviour until it becomes risky at scale.

Good regulation doesn’t prevent failure.

It tries to make failure survivable.

It slows things down.

It reduces the chance that everyone makes the same mistake at the same time.

And it tries — imperfectly — to stop private decisions automatically becoming public problems.

Which is why regulation keeps reappearing in this conversation.

Not as a moral crusade.

Just as an attempt to keep a fast system from running away with itself.

And where does that leave us?

Once we look at financial services this way, a few things become harder to unsee.

The system isn’t incomprehensible.

Shareholding didn’t become broken — it became faster.

Incentives reward behaviour that makes sense locally, even when it causes trouble globally.

And regulation isn’t anti-market.

It’s the cost of running markets at scale.

Because if the greatest trick finance ever pulled was convincing us we wouldn’t understand it…

…the second was convincing us that, this time, it would regulate itself.

History suggests that’s an optimistic assumption.

Discover more from Hysnaps Politics, Gaming, Music and Mental Health

Subscribe to get the latest posts sent to your email.